Financial considerations around deep-sea mining, which are central in the discussions on the draft exploitation regulations at the International Seabed Authority (ISA), dominated the day’s discussions. Such issues are technical and often complex, leading to an arduous day for delegates and observers alike.

Chair Olav Myklebust opened the session of the Working Group on the financial terms of a contract, inviting delegates to resume Monday’s discussions on incentives (Regulation 63).

Delegates focused on whether non-financial incentives can be included and, if so, the nature of such incentives. A regional group stressed that financial incentives are consistent with the UN Convention on the Law of the Sea (UNCLOS) and can only be provided for the goals of the Enterprise and technology transfer. A member stated that technology transfer should be an obligation, accompanied by personnel training, while others expressed divergent opinions on compulsory technology transfer.

On the issue of the commencement of commercial production (Regulation 27), a member provided an overview of a proposal submitted at the 28th annual session last year. He emphasized that the period of commencement of commercial production should be based on the maintenance of a certain level of production capacity for a specified number of days in accordance with the applicable standard, suggesting 60% of the initial capacity for 90 consecutive days.

Some members supported the proposal, suggesting using 80% of the initial capacity as the threshold. Delegates further queried whether: a contractor may take advantage of the threshold to delay payment of royalties; a reference to “reasonable efforts” to bring each mining area into commercial production could lead to subjectivity; and coastal states should be notified.

The working group discussed the transfer of rights and obligations under an exploitation contract (Regulation 23) with a particular focus on the transfer of profit share. Delegates expressed their views on, among other things: the necessity for such provision; the relevant land-based mining practice; the origin of the mandate or power of the ISA to receive these profit shares; and the relationship between profit shares and royalties.

On books, records, and samples (Regulation 39), delegates expressed divergent opinions on the need for bookkeeping to contain information on revenue and liabilities. Some suggested keeping language, as a standalone provision, on keeping books, accounts, and records at a mutually agreed place, to be available for inspection.

Chair Myklebust encouraged informal discussions to reach consensus and closed the morning session.

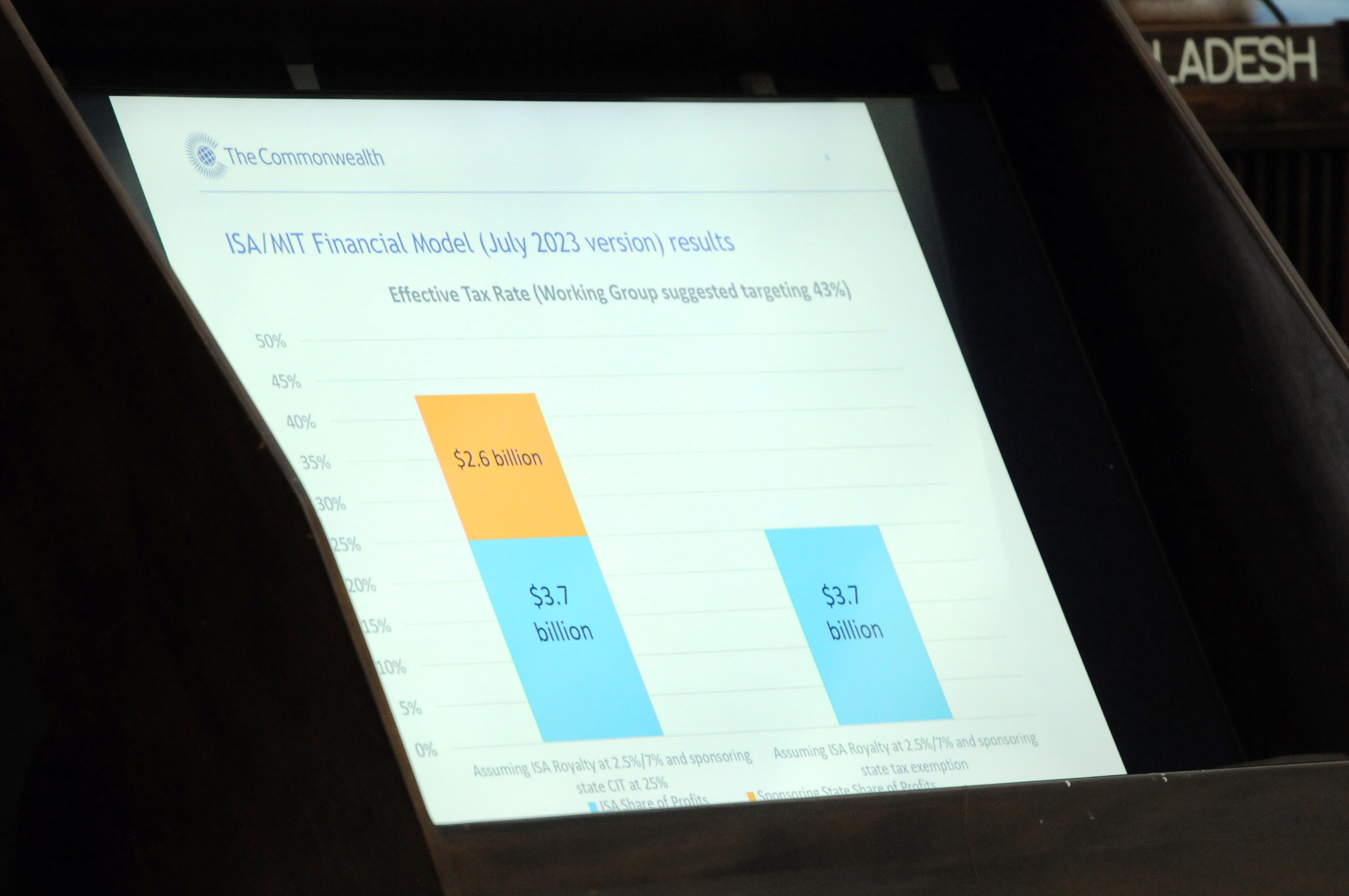

In the afternoon, delegates engaged in a thematic discussion on equalization measures, facilitated by Robyn Frost, Australia, aiming to address cases where contractors pay different sponsor state corporate income tax.

Following an overview of the discussions on an equalization measure under the auspices of the Working Group on the financial terms of a contract, including during the last intersessional period, Daniel Wilde, Commonwealth Secretariat, offered a comprehensive presentation focusing on, among other things:

- the meaning of an effective tax rate, including the relevant current range for land-based mining jurisdictions;

- the financial model calculating the effective tax rate, including different options; and

- how an equalization measure would work, including shortlisted options and key benefits.

In the ensuing discussion, delegates generally supported an equalization measure to ensure a level-playing field between deep-sea and land-based mining. They discussed, among other things: whether subcontractors are considered in the proposed equalization measure options; how equalization measures apply in the case of the Enterprise and state-owned companies; and the differences between tax equalization measures and the incorporation of environmental externalities in the financial model.

The Working Group on the financial terms of a contract then resumed its deliberations.

On audit by the ISA (Regulation 75), delegates discussed whether the Council or the Secretary-General should appoint an independent auditor.

On assessment by the ISA (Regulation 76), discussions focused on the process for assessing any royalty liability. Delegates exchanged views on a provision where the Secretary-General is expected to reconsider and either affirm, revise, or revoke the assessment.

Members agreed that the annual fixed fee (Regulation 85) should be paid to the ISA from the date of commencement of commercial production. On the interest on unpaid royalty (Regulation 79), a member suggested adding a penalty in case of non-payment.

Some members suggested deleting Regulation 80 on monetary penalties, noting it is already addressed under Regulation 103 (compliance notice, suspension, and termination of exploitation contract).

Discussions in the working group will continue Wednesday.

In the evening, a side event hosted by Germany addressed the environmental costs of deep-sea mining.

To receive free coverage of global environmental events delivered to your inbox, subscribe to the ENB Update newsletter.

All ENB photos are free to use with attribution. For the 1st Part of the 29th Annual Session of the ISA, please use: Photo by IISD/ENB | Diego Noguera

Open-ended Working Group on the Financial Terms of a Contract

The dais during the Working Group on the financial terms of a contract

Kim Jin-wook, Republic of Korea

Robyn Frost, Australia

José Benchetrit, Canada

Eden Charles, Interim Director-General of the Enterprise

Eduardo Sfoglia, Brazil

Esther Salamanca, Spain

Oliver Whitehead consults with Emma van den Boogaard, the Netherlands

Andy Aron, Indonesia

Helen Mulvein, UK

Cebert Mitchell, Jamaica

Duncan Muhumuza Laki, Uganda

Xi Mu Shi, China

Francis Winston Changara, Zimbabwe

Salvador Vega Telias, Chile

Helen Mulvein, UK, and Duncan Muhumuza Laki, Uganda

Maddyel Reyes, Cuba

Clemens Wackernagel, Germany

Livia Ermakova, Russian Federation

Michelle Walker, Jamaica

José David Sánchez Cedeño, Costa Rica

Youngdawng Moh, Republic of Korea

Bongani Sayidini, South Africa

(L-R) Matthew Gianni, Deep Sea Conservation Coalition (DSCC); María Ovalle, ENB; with Patricia Esquete and Samantha Robb, Deep Ocean Stewardship Initiative (DOSI)

Lowri Mai Griffiths, UK, and Duncan Currie, DSCC

Khadija Steward, Sustainable Ocean Alliance (SOA), and Pradeep Singh, International Union for Conservation of Nature (IUCN)

Thematic Discussion on Equalization Measures

Council members follow the thematic discussion on equalization measures

A slide from the presentation by Daniel Wilde, Commonwealth Secretariat

Daniel Wilde, Commonwealth Secretariat

Richard Roth, Massachusetts Institute of Technology (MIT)

Elza Moreira Marcelino de Castro, Brazil

Matthew Gianni, DSCC

Observers follow the discussions

Evening Event: The Environmental Costs of Deep-Sea Mining

Pradeep Singh (right), RIFS-Helmholtz Centre Potsdam, Germany, moderates the Q&A session

Jan Hendrik van Thiel, Ambassador, Permanent Representative of Germany to the ISA

Moderator Pradeep Singh, RIFS-Helmholtz Centre Potsdam, Germany

Torsten Thiele, RIFS-Helmholtz Centre Potsdam, Germany

Daniel Wilde, Commonwealth Secretariat

Rashid Sumaila, University of British Columbia

Group photo at the end of the event

Around the Venue

Art exhibition around the Jamaica Conference Centre, venue of ISA-29

Anja Morris, Norway, and Maria Luís Mendes, Portugal

Delegates from China confer outside the meeting room