Improving current frameworks for tax cooperation involves decisions about whether to enhance existing frameworks, or to rebuild them to better suit the needs of Global South countries. This choice surfaced time and again during discussions of the draft Framework Convention on International Tax Cooperation.

While some countries welcomed the opportunity to reimagine how tax cooperation can improve domestic revenue collection and provide much-needed funds for sustainable development, others cautioned against abandoning principles around data protection and privacy. Nevertheless, the vision of a unified framework for tax cooperation remained strong as delegates resumed discussions on day 2 of negotiations.

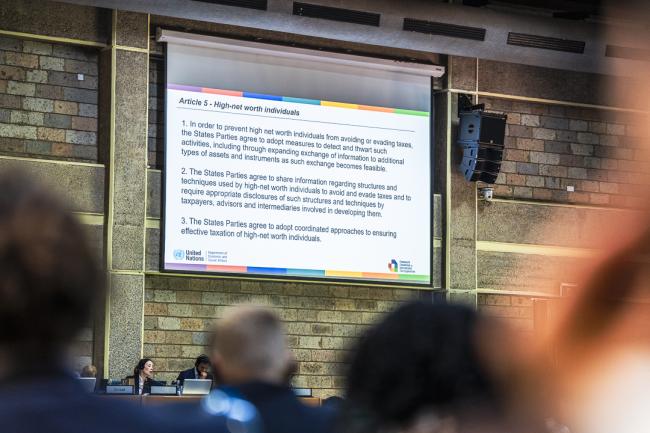

In the morning, delegates continued their review of Article 5 on high net-worth individuals (HNIs). Discussions focused on information exchange among countries. Practical solutions were proposed, such as establishing a global asset registry and compiling a database of countries’ measures to detect tax avoidance and evasion. Several developing countries warned against weakening the text, and the African Group called for deleting the qualifying phrase, “as such exchange becomes feasible.”

The Bombay Chartered Accountants' Society (BCAS) proposed reviewing what was achieved by the BEPS Action Plan 12 on Mandatory Disclosure Rules, implemented under the OECD/G20 Base Erosion and Profit Shifting Project. Delegates also noted possibilities for “automatic” information exchange. The discussion concluded with a call for definitions of HNIs and exploration of the implications of automatic exchange.

The focus on information exchange continued under discussion of Article 6 on mutual administrative assistance. The African Group proposed broadening the scope of administrative assistance to include “tax collection, simultaneous tax examination, tax examination abroad, service of documents or any other assistance as the conference of the parties (COP) determines.”

Peru called for a common standard on confidentiality, and Saudi Arabia proposed introducing a separate article on confidentiality. Several delegates, including France, China and Saudi Arabia, expressed unease regarding a reference to collection of tax debts, saying this should remain a domestic issue.

A common concern was the potential overlap of the Framework Convention with existing frameworks, especially the OECD Convention on Mutual Administrative Assistance in Tax Matters (MAAC). Japan, with many others, said it will be more beneficial to improve existing frameworks. Belgium said this could be done with a view to focusing on the problems that developing countries face regarding current frameworks.

In the afternoon, the meeting addressed Article 7 on illicit financial flows, tax avoidance, and tax evasion. The EU highlighted the distinction between tax evasion, which is illegal, and tax avoidance, which is not. They noted that it could be difficult to discourage actions that are “against the spirit” of taxpayer responsibility but are not, strictly speaking, against the law. Others observed that these concepts may have different meanings in different contexts, and agreed that having a clear definition of the three concepts is critical to avoid inconsistency.

Toward the close of the day, the Tax Justice Network reminded delegates of “the ABCD of tax transparency”, which refers to the automatic exchange of information, beneficial ownership registration, country-by-country reporting, and disclosure of sufficient public data and enforcement by well-resourced tax authorities. They welcomed the possibility of moving away from “a patchwork of reforms” to adopting a unified framework for international tax cooperation.

To receive free coverage of global environmental events delivered to your inbox, subscribe to the ENB Update newsletter.

All ENB photos are free to use with attribution. For the International Tax Cooperation INC3, please use: Photo by IISD/ENB | Danny Skilton.

Plenary

Syama Saji, India

Mathew Gbonjubola, Nigeria

Alexander Smirnov, Russian Federation

Juma Mkabakuli, Tanzania

Jiveon Oh, Republic of Korea

Civil society delegates huddle during a break

Richard Tolson-Pile, UK

Wanjiru Kiarie, Kenya

Gerald Namoma, Uganda

Guillaume Lecaros-de-Cossio, Peru

Setsoto Ranthocha, Lesotho

Christine Wachira, Global Impact

Patricia Mworozi, Akina Mama wa Afrika (AMwA)

Anne Wanyagathi Maina, South Centre

Nathalie Beghin, Institute of Socioeconomic Studies

Daniel Atwere Nuer, Ghana, Workstream 1 Co-Lead

Around the Venue