Tax cooperation among nations goes back a long way — as Jamaica reminded delegates, “This work has been done for more than 100 years, even before some of us were sovereign states.” Crafting a new multilateral agreement on tax cooperation thus raises many questions about how its provisions will interact with existing arrangements.

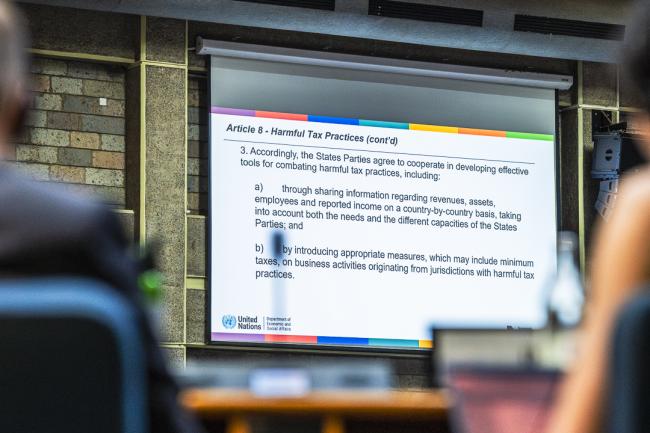

Discussions on the third day of negotiations addressed several articles of the future Framework Convention beginning with Article 8 on harmful tax practices. Many delegates called for clear definitions of terminology. They debated whether or not to mention examples and remedies to harmful tax practices, such as introducing “minimum taxes.” The Bahamas, among others, objected to this reference, expressing concern that current approaches to defining a harmful tax practice are discriminatory and inequitable with regard to low- or no-tax jurisdictions.

Tanzania said decisions on what constitutes a harmful practice continue to be made in settings where countries, especially those in Africa, have little or no decision-making power. They stated that developing countries legitimately use tax incentives to promote industrialization and job creation.

Kenya and many other countries of the Global South emphasized that “not all countries benefit” from existing arrangements. Others called for identifying where current arrangements fall short. Brazil highlighted that many countries do not participate in existing fora, and could benefit from the expanded scope of cooperation that a new convention could offer. This, they said, could create political momentum and help countries justify changes in their domestic legislation.

Some proposed “exploring” rather than “developing” effective tools to combat harmful tax practices, in view of countries’ differing capacities.

Delegates also discussed Article 9 on sustainable development. Some countries approved the brief text on pursuing international tax cooperation that will contribute to the achievement of sustainable development in terms of its economic, social, and environmental dimensions. Others called for expanding the text to include relevant concepts and enablers, such as domestic resource mobilization and human rights considerations.

Civil society representatives emphasized that the current meeting is more than a technical tax negotiation, stressing that the discussions are also making choices in terms of how to address the climate and inequality crises. They noted that “tax systems are not neutral” and that the current architecture is rooted in colonial structures that concentrate wealth while depriving women and marginalized communities.

At the close of the day, Co-Lead Daniel Nuer (Ghana), introduced Article 10 on the prevention and resolution of tax disputes. Patricia Brown, INC Secretariat, presented examples of disputes that could be covered under Article 10, including on cross-border transfer pricing (covered under Article 9 of the UN Model Double Taxation Convention), and the settlement of domestic tax disputes with cross-border implications. She also presented examples of issues that could be covered under Article 20 of disputes between governments, specifically related to confidentiality of tax information.

Following requests from several Member States, the meeting adjourned to allow delegates time to reflect on the presentations before engaging in further discussion.

To receive free coverage of global environmental events delivered to your inbox, subscribe to the ENB Update newsletter.

All ENB photos are free to use with attribution. For the International Tax Cooperation INC3, please use: Photo by IISD/ENB | Danny Skilton.

Plenary

Veronika Daurer, Austria

Sheriff Kamara, Sierra Leone

Qiaolang Li, China

Saleh Niazi, Iran

Hajara Batamuliza, Rwanda

Helen Pahapill, Estonia

Anne Myra van der Meulen, the Netherlands

Ricardo Augusto Gil Reis Rodrigues, Brazil

Ami-Jade McCarthy, Greenpeace International

Lurit Yugusuk, Children and Youth International (CYI)

Around the venue

A group photo of INC3 participants