Dispute prevention and resolution are essential to the effective implementation of treaties. Such mechanisms can be both high-level as well as detailed. Discussions on the fourth day of INC3 sought to make sense of how such arrangements may be spelled out in the new Framework Convention.

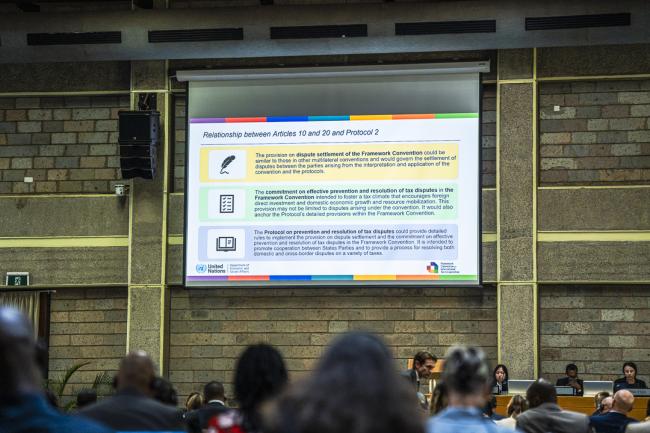

Resuming discussion of Article 10 on prevention and resolution of tax disputes, Daniel Atwere Nuer (Ghana), Co-Lead for Workstream 1 on the draft Framework Convention, reminded delegates that Article 10 is “the foundation” for other provisions. He explained that Article 10 is intended to govern the settlement of disputes between the parties arising from the interpretation and application of the Convention and its Protocols, whereas Article 20 on settlement of disputes under the Convention, to be drafted for review at the next INC, is about disputes that could arise. He noted that Protocol 2 on prevention and resolution of tax disputes, to be developed under Workstream 3, will provide “the rules.”

Delegates questioned the reference that States Parties’ will strive to implement “domestic” dispute resolution mechanisms. Many countries—including Brazil, China, India, Spain, and Morocco—suggested deleting this reference. Zambia, for the African Group, proposed replacing “domestic” with “appropriate.” India and others called for stating the kinds of disputes that will be settled under Article 10.

Chair Ramy M. Youssef (Egypt) said the text provided a base to show that the COP of the new Framework Convention could provide examples of best practice and guidelines. Norway, Germany and several others said that both domestic and international contexts should be considered.

The African Union emphasized that the resolution of tax disputes improves outcomes in general. They noted the need to define the scope of cases to be addressed under Protocol 2. Ireland and other countries called for a further discussion of Article 10 together with Article 20 on settlement of disputes arising under the convention.

The African Women’s Development and Communications Network (FEMNET) underlined the value of dispute prevention as being more equitable and less costly than dispute resolution.

Following Article 10 discussions, Chair Youssef opened the floor for general comments.

Referring to the previous day’s discussion of Article 9 on illicit financial flows (IFFs), India drew attention to the UN Statistical Commission’s work on Sustainable Development Goal (SDG) indicators, including measurement of IFFs (SDG indicator 16.4.1).

The Bahamas called for addressing “tax avoidance” in a separate article, so as to distinguish it from the illegal practice of tax evasion. Uganda suggested State Parties could publish their decisions with regard to how certain cross-border matters have been resolved, for the information of other States.

Chair Youssef then gave a preview of the elements that could be relevant when drafting Article 11 on Capacity Building and Technical Assistance, to be presented at the next INC meeting. He invited delegates’ views on whether capacity-building should be addressed in a stand-alone article, or if specific clauses should be inserted in other substantive articles, so as to directly link their implementation to the provision of support for capacity-building.

The African Union noted Article 11’s crucial importance to ensure effective implementation and called for consolidating all aspects of capacity-building in one article. They stressed that support “must be comprehensive enough to match the vision.”

Many countries supported having a stand-alone article on capacity-building—among them Egypt, Zambia, the UK, Jamaica, Sweden, Mauritius, Sierra Leone, and the Bahamas. The Bahamas noted the limited human resource capacity of small island developing states.

Following the lunch break, Member States convened in a closed plenary session.

Chair Youssef announced the open plenary would reconvene on Friday morning to resume discussions.

To receive free coverage of global environmental events delivered to your inbox, subscribe to the ENB Update newsletter.

All ENB photos are free to use with attribution. For the International Tax Cooperation INC3, please use: Photo by IISD/ENB | Danny Skilton.

Plenary

Gary Hynds, Ireland

Marlene Nembhard Parker, Jamaica

Cezary Krysiak, Poland

Ignatius Mvula, Zambia

Ghania Rabhi Mansour, Algeria

Robert Mwale, Centre for Trade Policy and Development

Donata Dionisi, Italy

Qiaolang Li, China

Fahd Loubaris, Morocco

Juma Mkabakuli, Tanzania

Ahtesham Khan, Advisor, International Cooperation and Tax Policy, FSDO/UNDESA

A UNON conference services staff member keeps watch outside the closed afternoon session

Around the venue