The purpose of an equalization measure is to ensure that the effective tax rate for deep-sea mining is on par with the rate for land-based mining, regardless of tax exemptions provided by sponsoring states. They help create a level playing field between deep-sea and land-based mining.

On day 2 of the second part of the Council of the 30th annual session of the International Seabed Authority (ISA), the informal working group on equalization measure considered two equalization options: a hybrid model, where contractors that receive tax exemptions or subsidies pay an additional 8% royalty to the ISA, against which payments to the sponsoring state are creditable; and a profit share option, where contractors pay 25% of their profit to the ISA, from which royalty payments to the sponsoring state and all mining payments by related entities are credited. Most Council Members expressed support for the profit share option.

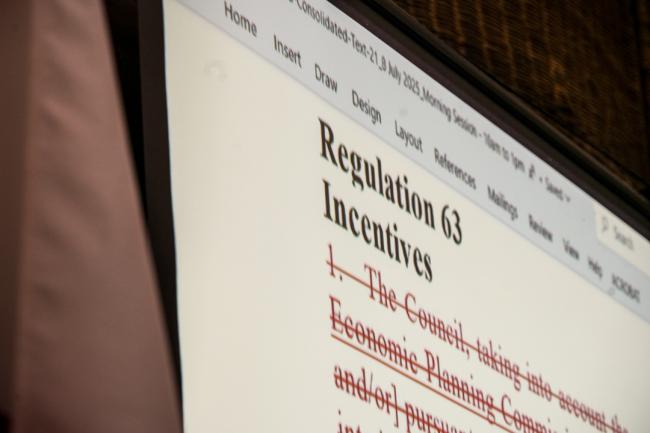

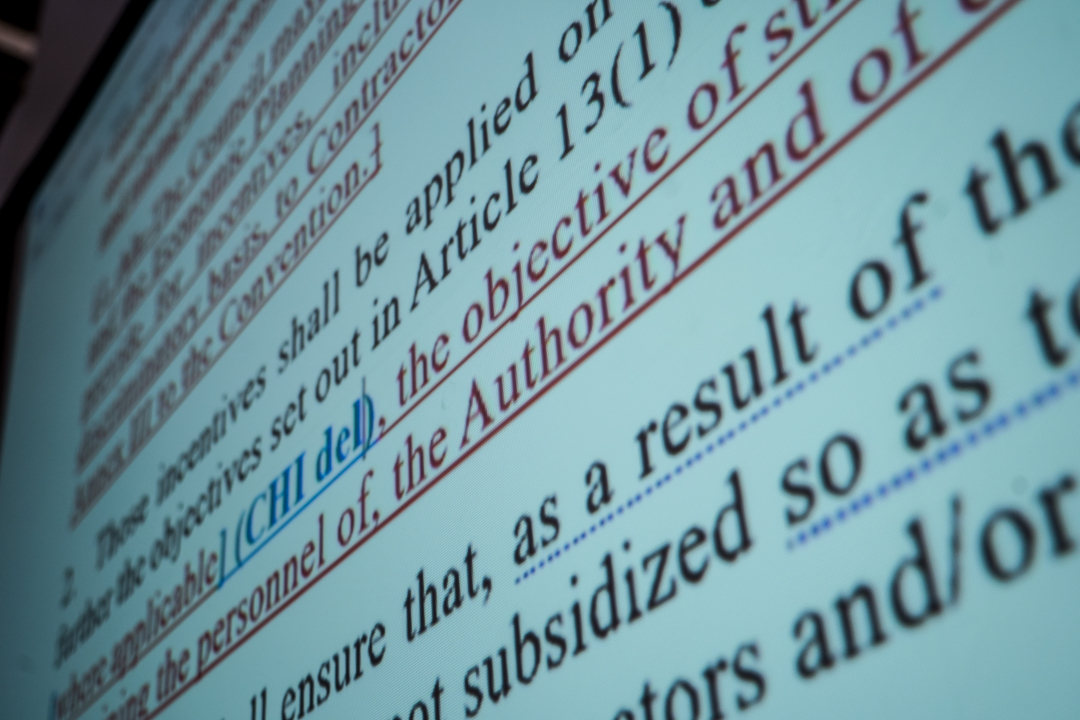

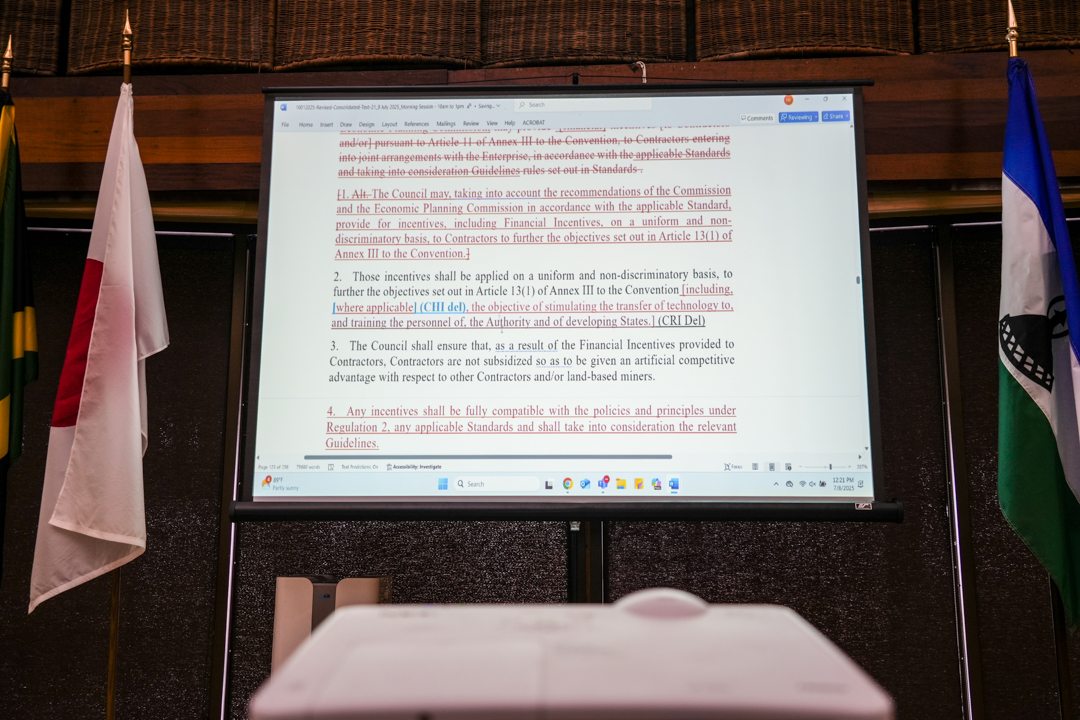

Throughout the day, delegates continued discussing the draft regulations for commercial exploitation of deep-sea mineral resources. Many Council Members argued for deleting regulation 63 (incentives), questioning, among other things, why contractors should be given incentives to comply with their contractual obligations. They cautioned this may create an unnecessary burden for the ISA and result in unequal conditions compared to land-based mining.

On regulation 64 (royalty payments), several delegates supported reinstating paragraphs relating to additional royalties to cover environmental externalities and costs, such as the future value of marine genetic resources, existence and bequest values for remote and unknown biodiversity, carbon emissions, and impacts on carbon sequestration by benthic and pelagic ecosystems.

Delegates considered and provisionally agreed to regulations 66 (form of royalty returns), 67 (royalty return period), 68 (lodging of royalty returns), and 69 (error or mistake in royalty return). Regarding regulation 70 (payment of royalty shown by royalty return), most delegates opposed reference to contractors determining the currency to be used in the payment of royalties, stressing this choice should not be left to contractors.

On regulation 73 bis (underpayment of royalty), a Council Member proposed, and many others supported, reverting to previous language that “where a royalty return shows any underpayment of royalties, the contractor shall pay within 7 days from the notification of the Secretary-General.”

Several delegates proposed deleting regulation 75 (audit by the Authority), noting its content is covered by regulation 96 (the inspection mechanism). Some noted that the regulation title is misleading since the audit is undertaken by an independent auditor and not the Authority. Discussing regulation 78 (arm’s-length adjustments), one Member suggested that operations by state-owned enterprises should be considered non-arm’s-length by default and proposed text to this effect.

Delegates agreed to delete regulation 80 (monetary penalties) and to instead, address monetary penalty issues in regulation 103 (non-compliance, notice, suspension, and termination of exploitation contract). They also accepted an alternative proposal for the seabed mining register (regulation 83).

On regulation 83 bis (beneficial ownership registry), several Members emphasized the need to define the beneficial ownership registry and to also include it in regulation 7 (form of applications and information to accompany a plan of work).

Discussions on regulation 84 (annual reporting fee) considered the timelines for payment of annual reporting fees, with delegates noting that the payment is due from the date of signing the exploitation contract. A participant called for reference to the fee exemption granted to the Enterprise during the initial period required for it to become self-supporting.

To receive free coverage of global environmental events delivered to your inbox, subscribe to the ENB Update newsletter.

All ENB photos are free to use with attribution. For the Second part of the 30th session of the International Seabed Authority (ISA) Council meeting, please use: Photo by IISD/ENB | Andrés Felipe Carvajal Gómez

Informal Working Group on Equalization Measure

Observers listening to the deliberations

Chinese Delegation

María Ovalle, ENB

View of the room

Delegates during the informal working group on equalization measure

Makiko Murai-Ikegami, Japan

Oliver Whitehead, the Netherlands

Selected Images

Eden Charles, Interim Director-General of the Enterprise

Around the Venue